This practical guide demystifies the process. We’ll explain the legal and financial steps, clarify who does what, and provide clear checklists so you can navigate your closing with confidence. While the article is detailed, it’s organized with quick-jump links to the sections that matter most to you.

The big picture: what “closing” actually means

A closing is the legal transfer of ownership and money, and the registration of rights and obligations. In every province, lawyers or notaries coordinate funds, confirm title, register transfers and security, and release keys or possession. There is usually no in-person ceremony. Most actions occur between law offices, lenders, and registries. Quebec typically uses notaries. Ontario, B.C., Alberta, and others use lawyers and electronic land registration systems.

Core ingredients of any closing

- Signed purchase agreement and all amendments

- Satisfied conditions, including financing and insurance

- Verified title and searches

- Final money flow, including adjustments and taxes

- Registration and delivery of possession or control

- Post-closing reports and records

Your Closing Team: Who Does What?

A successful closing is a coordinated effort. Here are the key players and their primary roles:

- Your Lawyer or Notary (The Quarterback): This is your primary representative. They review all documents, conduct title searches, coordinate with the lender, calculate the final flow of funds, register the transfer, and ensure your legal interests are protected.

- The Lender (The Funder): The bank, credit union, or private lender provides the mortgage funds. Their lawyer or internal department sends the funds to your lawyer’s trust account only after all funding conditions are met.

- The Real Estate Agents (The Coordinators): Your agent (and the other party’s agent) are the logistical hubs. They coordinate the final walkthrough, manage the physical key handover, and are the first point of contact for any last-minute property condition issues.

- The Title Insurer (The Protector): (This is often arranged by your lawyer). This company provides a policy that protects you and your lender from future title-related issues, such as fraud, survey errors, or unknown municipal work orders.

- The Seller & Buyer (The Principals): Your main job is to sign the documents, provide the necessary funds (for the buyer), and provide vacant possession (for the seller) as agreed.

(For income property, tenants and property managers may also be involved through notices, estoppels, and rent directions.)

Key differences that change the closing experience

- Property type: freehold, condo, multi-residential, mixed-use, industrial, office, retail

- Deal structure: asset purchase vs share purchase in commercial

- Stage: resale vs pre-construction

- Occupancy: vacant vs tenant-occupied

- Province: registry mechanics, tax names, notarial vs lawyer system

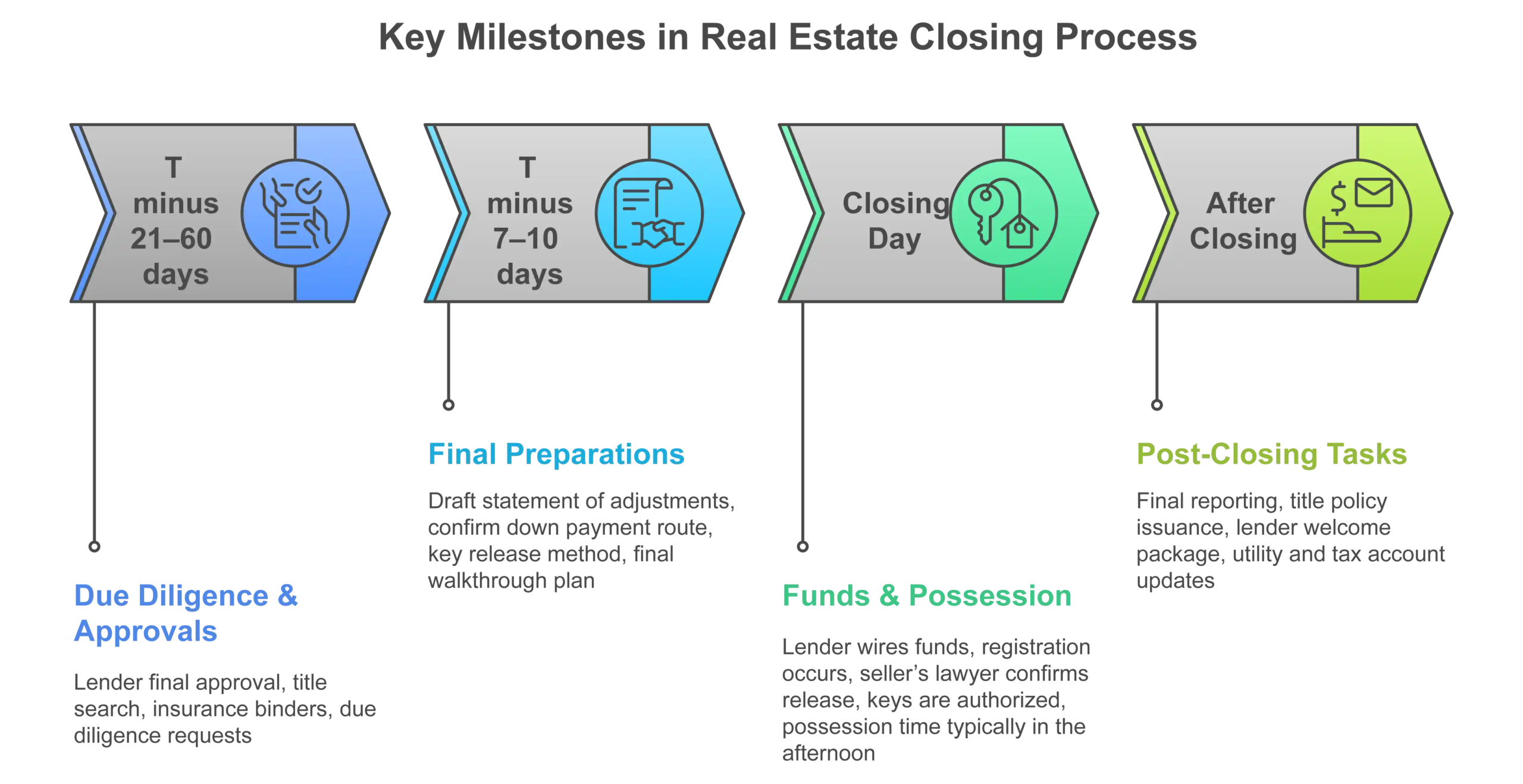

Standard timeline from firm deal to possession

- T minus 21–60 days: lender final approval, title search, insurance binders, due diligence requests.

- T minus 7–10 days: draft statement of adjustments, confirm down payment route, key release method, final walkthrough plan.

- Closing day: lender wires funds to buyer’s lawyer, registration occurs, seller’s lawyer confirms release, keys are authorized, possession time typically in the afternoon.

- After closing: final reporting, title policy issuance, lender welcome package, utility and tax account updates.

Following the Money: The Statement of Adjustments & Closing Costs

The financial core of the closing is the Statement of Adjustments. This is the official ledger prepared by the seller’s lawyer and verified by the buyer’s lawyer. It balances the books between both parties, ensuring everyone pays their fair share up to the exact closing date.

How the Statement of Adjustments Works

The statement starts with the purchase price and then adds or subtracts costs.

- Credits to Buyer:

- The deposit you already paid.

- Prorated property taxes (if the seller prepaid for a period you will own the home).

- Prorated condo fees (if the seller prepaid).

- Debits to Buyer (Costs Added to the Price):

- The remaining purchase price.

- Prorated property taxes (if the seller has not yet paid the amount due).

- Prorated utilities in some cases (e.g., heating oil).

Typical Closing Costs (The ‘Costs to Close‘)

These are the expenses you pay in addition to the purchase price. Your lawyer will provide a final “trust ledger” showing exactly how much money to bring in.

For Buyers:

- Land Transfer Tax (LTT): The largest closing cost. Remember, Toronto has both a provincial (Ontario) and a municipal (Toronto) LTT.

- Legal Fees & Disbursements: The fee for your lawyer's services plus their hard costs (couriers, searches, etc.).

- Title Insurance: A one-time premium, usually a few hundred dollars.

- Registration Fees: The government fee to register the deed and mortgage.

- Home Insurance: You must have a fire insurance "binder" in place before the lender will send funds.

- Adjustments: The final amount owed from the Statement of Adjustments.

For Sellers:

- Real Estate Commission: As per your listing agreement.

- Legal Fees & Disbursements: To prepare the deed, review documents, and pay off your mortgage.

- Mortgage Payout & Discharge Fee: The cost to pay the remaining mortgage balance plus any prepayment penalty and a bank fee to remove the charge from title.

Risk controls that prevent last-minute problems

- Title insurance to backstop registration defects or certain frauds

- Bringdown searches on closing morning to catch new liens or writs

- Clear, written key release conditions to avoid possession disputes

- Bridging or extended funding windows if there are back-to-back sales

- Holdbacks where there is unfinished work, missing documents, or measured environmental or construction risk

Special note on tenant-occupied purchases

If a buyer will keep tenants, expect tenant notices, estoppel certificates, and rent direction letters, plus proration of rent, deposits, and last month rent credits. If the buyer requires vacant possession, the seller must deliver it as per contract and local law, which often requires specific notices and lead times.

Documentation you will see, regardless of property type

- Statement of Adjustments

- Direction re Funds and undertakings between law firms

- Transfer/Deed and mortgage or charge

- Title insurance policy or solicitor’s opinion on title

- Tax certificates, utility confirmations, or condo status documents

- Proof of insurance effective on closing

Identification attestation, anti-money-laundering verifications.

Residential Closing

This section covers freehold houses, townhomes, condos, and resale vs pre-construction.

What changes in residential compared with commercial

Residential focuses on consumer protection, mortgage funding predictability, and possession logistics. Commercial focuses more on leases, environmental risk, and corporate documents. Residential buyers usually care about keys, utilities, and fixtures. Commercial buyers care about income continuity, estoppels, and operational risk.

Freehold vs condo

- Freehold: land and building transfer as one parcel. You reconcile property taxes and sometimes oil tank or well documentation in specific regions.

- Condo: unit transfer plus common interest. Expect a Status Certificate review for budgets, reserve fund studies, special assessments, and rules. Adjustments include condo fees, parking, and locker where applicable.

Resale vs pre-construction

- Resale: single closing for title and possession.

- Pre-construction condo: often two stages in Ontario and several provinces.

- Occupancy (interim): buyer takes possession before title exists. Buyer pays occupancy fees to the builder.

- Final closing: title is registered when the condominium is declared. Land transfer tax and the mortgage register here.

Pre-construction freehold can also involve builder holdbacks, Tarion or provincial warranty enrollments, and new home HST considerations.

The HST Factor: New vs. Resale

- Resale Homes: Used residential properties (houses, condos) are exempt from HST.

- New Construction Homes: HST is always payable on new construction. The price from a builder often includes the HST, "net of" the federal and provincial new home rebates. Your lawyer's job is to ensure you qualify for these rebates, which are typically assigned back to the builder on closing. If you plan to rent out the new property, the rebate rules change, and you may need to pay the full HST upfront and apply for a different rebate (the "New Residential Rental Property Rebate") after closing.

Residential buyer checklist

- Final lender conditions satisfied and insurance binder dated to completion

- Down payment and closing costs in liquid form, typically a bank draft or wire to your lawyer’s trust

- Title insurance or title opinion selected

- Final walkthrough booked within 24–48 hours to confirm condition, inclusions, and removals

- Utilities transfer requests submitted with possession date

- Keys pick-up instructions confirmed with your Realtor and lawyer

- If tenant-occupied, rent proration, deposit handling, and notices are in the closing package

Residential seller checklist

- Mortgage payout statement and discharge authorization delivered to lawyer

- Keys and fobs collected and labeled, remote controls and codes prepared

- Proof of repairs or compliance promised in the agreement, including permits or receipts

- Forwarding address for final utility bills and property tax reconciliation

- Condo sellers: status certificate supplied and any special assessment details disclosed and reflected in adjustments

- Vacant possession delivered if contracted

Common residential hiccups and fixes

- Late lender wire. Fix with a temporary key escrow instruction or bridge financing if there is an onward purchase.

- Walkthrough surprise. Resolve by amendment and a monetary holdback for incomplete items.

- Undisclosed rentals or hot water tank contracts. Cure through payout, assignment, or price credit on closing.

Commercial Closing

This section covers income-producing or business-use property, including multi-residential, retail, office, and industrial, and distinguishes asset purchase vs share purchase.

Asset vs share purchase

- Asset purchase: buyer acquires real property and selected contracts. Land transfer tax applies. Environmental and title risk is centered on the property.

- Share purchase: buyer acquires the company that owns the property. No land transfer tax in many structures, but you inherit corporate history, liabilities, and contracts. Diligence shifts toward corporate, tax, and financial statements.

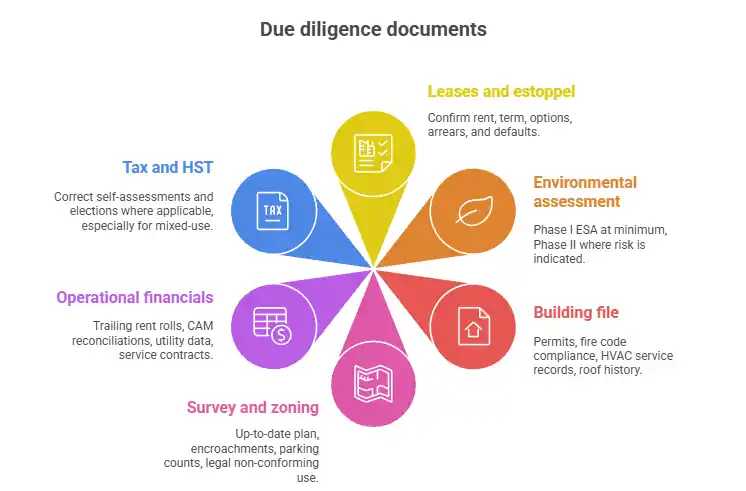

Due diligence that shapes commercial closings

- Leases and estoppel certificates that confirm rent, term, options, arrears, and defaults

- Environmental: Phase I ESA at minimum, Phase II where risk is indicated, reliance letters to lender

- Building file: permits, fire code compliance, HVAC service records, roof and envelope history

- Survey and zoning: up-to-date plan, encroachments, parking counts, legal non-conforming use where applicable

- Operational financials: trailing rent rolls, CAM reconciliations, utility data, service contracts

- Tax and HST: correct self-assessments and elections where applicable, especially for mixed-use

Commercial closing deliverables

- Assignment and assumption of leases, notices to tenants, and rent direction letters

- Non-disturbance agreements where lenders require them

- Bill of sale for chattels and equipment schedules

- Environmental reliance letters and representations

- Vendor declarations, corporate resolutions, bringdown certificates

- Holdback or escrow agreements tied to environmental, construction, or vacancy risk

Key Concept: The SNDA Agreement

When you buy a tenanted commercial property with a new mortgage, your lender will often require SNDA Agreements from key tenants. This stands for Subordination, Non-Disturbance, and Attornment.

- Subordination: The tenant agrees their lease is subordinate (secondary) to the new mortgage.

- Non-Disturbance: The lender agrees not to disturb the tenant (i.e., won’t evict them) if the landlord defaults on the mortgage, as long as the tenant keeps paying rent.

- Attornment: The tenant agrees to recognize the lender as their new landlord if the lender takes possession of the property.

Securing these from major ‘anchor’ tenants is a critical part of commercial closing diligence.

Typical commercial adjustments and money flow

- Base rent and additional rent prorations to the minute of completion

- Security deposits and prepaid rents credited to buyer

- Realty taxes and local improvement charges prorated

- Utilities, service contracts, and maintenance credits or debits

- Brokerage fees according to the listing or commission agreement

- Structured holdbacks for unresolved items, for example pending roof work or Phase II confirmation

Common commercial hiccups and fixes

- Estoppels not returned. Solve through seller certificates, targeted holdbacks, or rights to terminate if critical anchors are missing.

- Environmental flags. Insert conditional releases, indemnities, or price adjustments, and escrow for remediation.

- Rent roll mismatch. Require reconciliation of arrears with a price credit or tenant-by-tenant statement.

- Title gap. Cure with undertakings, corrective registrations, or insured over with specific endorsements.

You Have the Keys! What Happens After Closing?

Congratulations, you’re officially a property owner! However, the closing process isn’t quite finished.

What Your Lawyer Does Post-Closing

In the weeks after closing, your lawyer’s office is busy finalizing your file. They will:

- Pay Out Holdbacks: If any money was held back (e.g., for a repair), your lawyer will manage its release once conditions are met.

- Settle Final Undertakings: Complete any remaining administrative promises made to the other lawyer.

- Issue the Title Insurance Policy: You will receive the final, official policy document.

- Send a Final Report: You will receive a complete reporting package with copies of all registered documents, your statement of adjustments, and a final trust ledger. Keep this for your records.

Your New Homeowner Checklist

- Update Your Address: Immediately update your driver’s license, health card, banking, and any subscription services.

- Set Up Mail Forwarding: Arrange with Canada Post to forward mail from your old address.

- Review Your First Bills: Double-check your first property tax and utility bills to ensure the accounts were transferred correctly and the prorated amounts match your closing statements.

- Secure Your Home: Change the locks. You don’t know who the previous owner gave a spare key to.

Province-specific notes that affect expectations

- Quebec: notarial practice, different terminology for documents, and civil law concepts

- Ontario: Teranet registration, dual LTT in Toronto, frequent condo interim occupancy before title

- British Columbia: Property Transfer Tax, and additional forms for declarations

- Alberta: Land Titles Office timelines can affect registration time, plan wire windows accordingly

Final walk-through on expectations

- Closings are document-driven and mostly handled between professionals.

- Possession usually occurs after registration and confirmation of funds. Plan for an afternoon key release.

- Accurate adjustments and clear key release instructions prevent the most common disputes.

- For residential, focus on insurance, walkthrough, utilities, and inclusions.

- For commercial, focus on leases, estoppels, environmental, operating statements, and strategic holdbacks.

FAQs

Usually after registration and confirmation of funds, commonly mid to late afternoon. Your lawyer releases keys to your Realtor once undertakings are satisfied.

Typically no. Your signing and ID verification can be completed in advance, in person or by approved virtual methods, depending on province and lender.

Lawyers can use escrow instructions, short extensions, or bridging to avoid a failed chain, subject to contract terms.

Only if the contract allows early possession or rental-style occupancy, which is rare for resale and more common for pre-construction condos during the interim period.

Through lease assignments, estoppels, rent directions, and adjustments. If vacant possession is promised, the seller must deliver it in accordance with law and the agreement.