When people ask, “Is it better to rent or buy a house?”, they’re usually hoping for a simple financial calculation. If that’s you, Use our Rent vs. Buy Calculator to compare your specific scenario. But in Canada’s diverse housing market, the answer depends heavily on where you are and who you are.

Buying a condo in Calgary involves different laws, taxes, and closing costs than buying a rowhouse in Toronto or a detached home in Halifax. The “math” changes across provincial borders, but the core question remains the same:

- What kind of life do you want right now?

- How stable is your income?

- How do you feel about debt, repairs, and risk?

This guide walks through buying vs. renting from every angle, with a specific focus on the Canadian landscape:

- Psychological Factors in Homeownership: Why we feel the need to own.

- The Hurdles of Renting: Eviction risks, “Renovictions,” and rising rents.

- The Hurdles of Owning: The Mortgage Stress Test, property taxes, and the “house poor” trap.

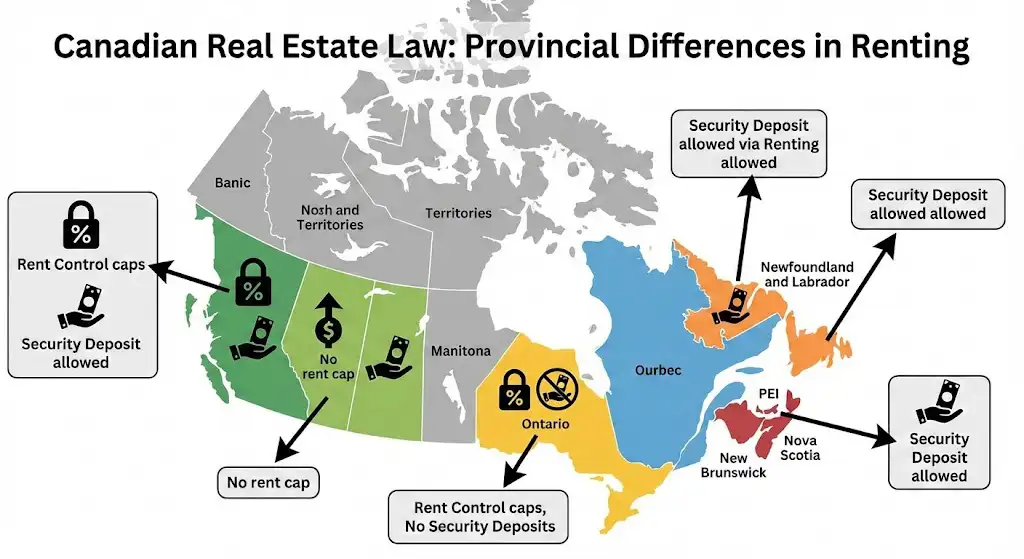

- Provincial Realities: “security deposit” is standard in BC but illegal in Ontario.

IMPORTANT: A Note on Provincial Laws (Ontario vs. The Rest of Canada) This guide provides general educational information only and is not financial or legal advice.

Real Estate laws vary significantly by province in Canada. While many examples in this guide reference Ontario’s Residential Tenancies Act (RTA), readers in other provinces must note key differences:

- Deposits: In Ontario and Quebec, “Security Deposits” (for damages) are generally illegal; landlords can typically only ask for the Last Month’s Rent (LMR). However, in British Columbia, Alberta, and the Atlantic Provinces, a “Damage Deposit” (often half a month’s rent) is standard and legally required.

- Rent Control: Ontario and BC have strict caps on annual rent increases for many units. In contrast, Alberta currently has no cap on how much a landlord can raise rent (provided proper notice is given).

- Closing Costs: Toronto has a double Land Transfer Tax (Municipal + Provincial). Most other Canadian municipalities do not.

Always consult a local real estate lawyer or mortgage broker for advice specific to your province and situation.

Why People Want to Buy a House

Before you compare rent vs buy, it helps to understand why homeownership is so emotionally loaded. People rarely buy purely because of spreadsheets.

1.1 Financial Reasons to Buy

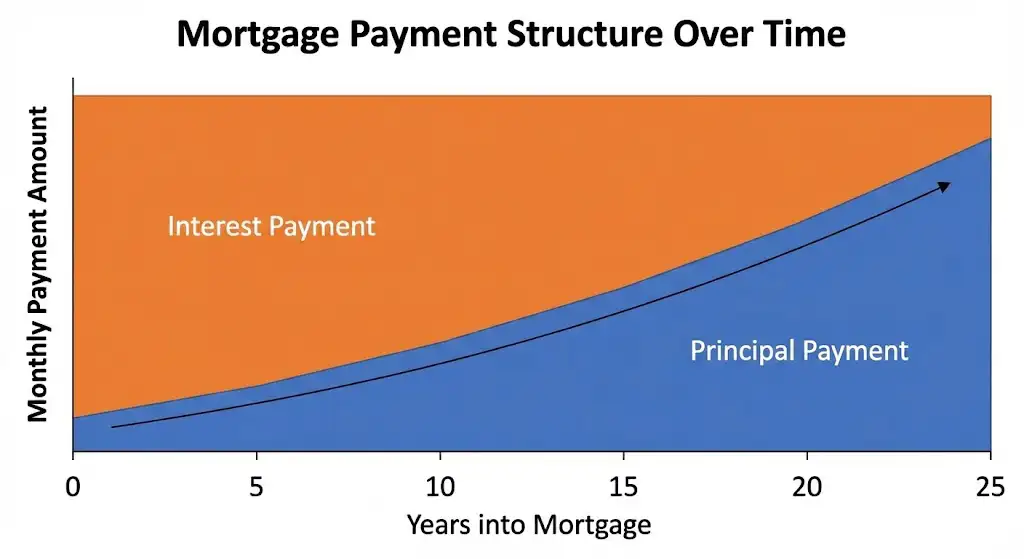

1. Build equity instead of paying rent

With a mortgage, each payment has:

- an interest portion (cost of borrowing), and

- a principal portion (which reduces what you owe).

Over time, the principal part grows, and that’s your equity. Renting never gives you that ownership stake.

2. Benefit from price appreciation

If home prices rise over the years, the owner — not the tenant — captures that gain. For many families, their home becomes their biggest single asset. Conversely, if values drop, the owner absorbs 100% of the loss, whereas a tenant walks away unharmed.

3. Hedge against rising rent

With a fixed-rate mortgage, your basic payment can stay relatively stable. “In non-rent-controlled units, rent can increase significantly. In controlled units, it typically increases by the provincial guideline annually. Owning can feel like long-term cost control, even if the first few years are more expensive.

4. Forced savings

A mortgage acts as a forced savings vehicle via principal repayment, though interest costs do not build equity.

5. Leverage (and the cost of it)

With 5–20% down, you control 100% of the property. If the home value rises, your return is based on the full price of the home, not just your down payment. Furthermore, as of December 2024, 30-year amortizations became available for all first-time homebuyers (and for buyers of new builds), not just those with 20% down.

Note: In Canada, if your down payment is less than 20%, you are required to purchase Mortgage Default Insurance (often called CMHC insurance). This protects the lender, not you, and the cost is added to your loan. It’s the price of admission for buying with a smaller down payment.

Down Payment Amount | Mortgage Default Insurance Premium Rate |

5% to 9.99% | 4.00% (The highest rate for the lowest down payment) |

10% to 14.99% | 3.10% |

15% to 19.99% | 2.80% (The lowest rate for high-ratio mortgages) |

6. Owner-Occupied Rental Strategies / house hacking

- Rent out a basement apartment, a room, or a secondary suite.

- Use that income to offset your mortgage.

Some people buy specifically to become small-scale landlords over time.

7. Retirement planning

Owning a home outright by retirement can lower housing costs when pay cheques stop. Some owners later sell and downsize, using the difference to help fund retirement.

8. Canadian Tax Advantages & Incentives

In Canada, the government provides specific tax shelters that make buying more efficient than just “saving cash”:

- The FHSA (First Home Savings Account): A game-changer introduced recently. You can contribute up to $8,000/year (up to a $40,000 lifetime limit) tax-free, and unlike an RRSP, you don’t have to pay it back when you buy. It combines the best of an RRSP and a TFSA.

- The Home Buyers’ Plan (HBP): This allows first-time buyers to withdraw up to $60,000 (as of the 2024 budget update) from their RRSPs tax-free to use for a down payment, provided it is paid back over 15 years.

- Principal Residence Exemption: In Canada, when you sell your primary home, the profit is generally 100% tax-free. This is one of the few unlimited tax shelters available to Canadians.

Disclaimer: “Subject to CRA rules (e.g., the Anti-Flipping Tax if sold within 12 months)

1.2 Stability, Security & Control

1. Security of tenure

You’re not dependent on a landlord deciding to sell, move back in, or raise rent. As long as you pay the mortgage, taxes, and upkeep, you generally decide when to move.

2. Long-term stability for family

- Kids stay in the same school

- You get to know neighbours

- You build routines and roots in one community

3. Control over your space

You can:

- Paint

- Renovate the kitchen

- Add storage or built-ins

- Keep pets (subject to local rules)

Without asking permission for every change.

4. Predictability of “home base”

Many people simply want to stop wondering, “Where will we live next year?” Owning often brings a sense of being settled.

1.3 Lifestyle & Space

1. More indoor space

- Extra bedrooms

- Home office

- Playroom

- Storage

- Hobby/workout room

Owning often means you can buy a layout that fits your life rather than accepting whatever rentals are available.

2. Outdoor space

A yard, deck, garden, or patio can be a big draw:

- Kids and pets can play outside

- You can host BBQs

- You can garden, relax, or just step into your own private space

3. Privacy

Fewer shared walls, less noise from upstairs/downstairs neighbours, your own driveway or garage, and more control over guests and noise.

4. Specific type of home

- Bungalow

- Side-split

- Multi-generational layout

- Secondary suite

- Accessibility features

Some configurations are easier to find in ownership than in rental inventory.

1.4 Family & Life-Stage Triggers

1. Marriage or long-term partnership

Couples often see buying as the next “grown-up” step after moving in together.

2. Having or planning kids

You may want:

- More bedrooms

- Bigger living areas

- A yard or safe outdoor play space

- A particular school catchment

3. Caring for parents / multigenerational living

A house with:

- Basement apartment

- Main-floor bedroom

- Separate entrance

can make it easier to care for aging parents while still having privacy.

4. Relocation for work

After a move and trial period in a new city, some people decide to buy to “plant roots.”

5. Retirement / downsizing

Selling a larger family home and buying a smaller, low-maintenance property can reduce costs and work, while freeing up equity.

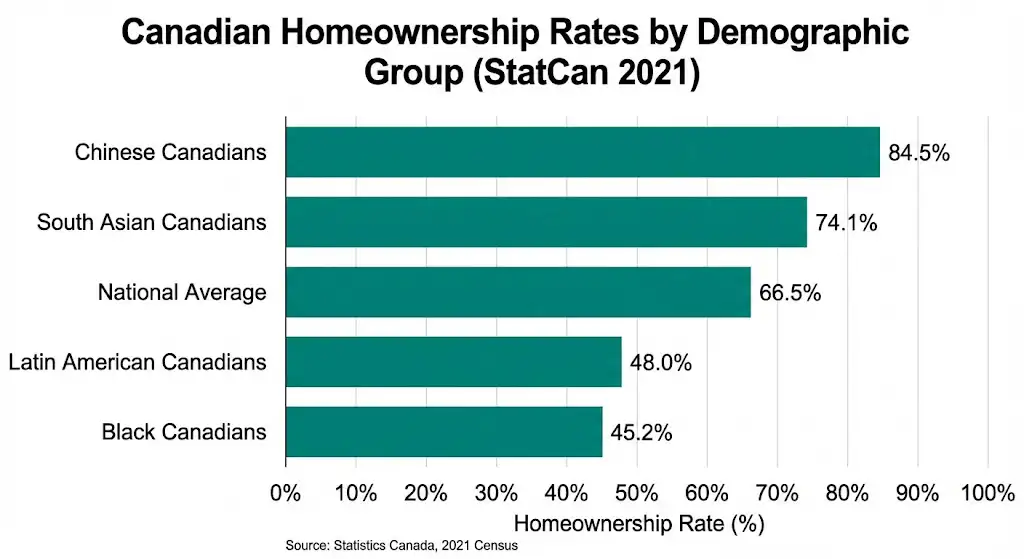

1.5 Who is Actually Buying? (Statistical Context)

According to Statistics Canada (2021 Census) data:

- The Age Gap: The homeownership rate for Canadians aged 25 to 29 dropped from 44.1% in 2011 to 36.5% in 2021. If you are under 30 and renting, you are in the majority.

- The Demographic Gap: Ownership rates vary significantly by community, highlighting systemic barriers. While the national ownership average is 66.5%, rates differ for various groups:

- Chinese Canadians: ~84.5%

- South Asian Canadians: ~74.1%

- Latin American Canadians: ~48.0%

- Black Canadians: ~45.2%

These numbers remind us that the “Rent vs. Buy” decision is often dictated by market accessibility, not just personal preference.

1.6 Psychological Factors in Homeownership

1. Sense of achievement

For many people, buying a house is part of the “life checklist”: school → job → relationship → home.

2. Identity & status

Owning can signal stability or success in some social circles. People may feel judged (rightly or wrongly) for renting long term.

3. Belonging & community

Ownership can deepen the feeling of belonging to a neighbourhood. People may be more likely to:

- Join school councils

- Get involved in local events

- Invest in long-term relationships with neighbours

4. Control over environment = peace of mind

Not worrying about a landlord’s decisions can reduce anxiety for some people. They feel more in control.

5. Legacy

Many want to leave a home to their children or family as a concrete inheritance.

1.7 Design, Customization & Accessibility

1. Make it feel like “you”

Custom finishes, built-ins, smart-home tech, and layout tweaks can make a home reflect your tastes and needs.

2. Accessibility or special needs

- Ramps

- Wider doors

- Accessible bathrooms

- Sensory-friendly layouts

Owners have more freedom to make these changes without landlord approval.

3. Energy efficiency & comfort

Investing in:

- Better insulation

- High-efficiency heating/cooling

- New windows

- Possibly solar

can improve comfort and (over the long term) lower bills.

1.8 Location, Schools & Community

1. Access to specific schools

Buying in a certain catchment area is often driven entirely by education priorities.

2. Proximity to work or transit

Shorter commutes, walkability, easy access to transit hubs — all can be big motivators.

3. Neighbourhood lifestyle

Some want quiet cul-de-sacs; others want lively urban streets, cafés, nightlife, or walkable neighbourhoods.

4. Long-term community ties

People may buy near family, friends, or cultural/religious communities to keep those networks close.

1.9 Less-Healthy Reasons to Buy (But Still Real)

1. “Everyone else is doing it”

Peer pressure.

2. FOMO (fear of missing out)

“If I don’t buy now, I’ll never get in.”

3. Family expectations

Parents or extended family insisting that “renting is throwing money away,” even when renting might be smart in a specific situation.

4. Social media / HGTV effect

Renovation shows and Instagram houses make ownership look glamorous and inevitable.

Why People Choose to Rent a House

On the flip side, renting is not just a “consolation prize.” There are very rational reasons to choose renting versus buying.

2.1 Financial Reasons to Rent

1. Much lower upfront cost Usually requires:

- First and Last Month’s Rent (LMR).

- A refundable key deposit (must be notional, e.g., cost of replacement).

Important: Security deposits for damages are illegal in Ontario, though a Rent Deposit (LMR) is standard.

This is significantly less capital than a 5–20% down payment plus closing costs.

2. No surprise repair bills

Roof leaks, furnace failure, plumbing issues — typically the landlord’s problem, not yours.

3. No property taxes or condo fees

Owners pay these. Renters usually don’t, at least not directly.

4. Money stays liquid

Instead of tying up tens or hundreds of thousands in a house, renters can:

- Invest in markets or a business

- Maintain a big emergency fund

- Pay down high-interest debt

5. Avoid housing market risk

If prices fall, renters don’t lose equity. You’re paying for shelter only, not gambling on property values.

6. Sometimes cheaper monthly than owning

Especially in high-price or high-interest environments, renting the same kind of home can cost less per month than owning it with a mortgage.

7. Access to expensive areas

You might be able to rent in a premium neighbourhood you could never afford to buy in.

8. Other means of Investment

Historical stock market returns (S&P/TSX) have often rivaled or outperformed real estate appreciation over long horizons.

2.2 Flexibility & Freedom to Move

1. Easy relocation

For moving due to:

- Job changes

- School

- Relationships

- Immigration status

Renting makes it much easier to pick up and move.

2. Short or uncertain time horizons

If you only plan to stay in a city for 1–3 years, buying vs renting a home usually tilts heavily toward renting once you factor in house transaction costs.

3. Testing a neighbourhood or city

Rent first, see if you like the commute, schools, noise, lifestyle. Buy later if it fits.

4. Students, interns, contract workers

If your life is naturally short-term or mobile, renting is usually a better match.

2.3 Lower Responsibility & Mental Load

1. No major maintenance responsibilities

Yard, snow removal, roof, windows, mechanical systems — often handled by the landlord or property manager.

2. Fewer long-term “house projects”

No endless list of renos or upgrades tugging at your time and wallet.

3. Less administrative hassle

No property tax bills, no condo board politics, no special assessments.

2.4 Lifestyle & Space Trade-offs

1. House lifestyle without long-term commitment

Renting a house (rather than a condo) can give you:

- Backyard

- Extra space

- Bedrooms

Without a 25-year mortgage.

2. Access to amenities

Some rentals have shared amenities (pools, gyms, community centres) built into the rent.

3. Bigger or nicer home than you could buy

In some markets, it’s possible to rent a larger or newer house than what you could realistically afford to purchase.

4. Try different living styles

City vs suburb, condo vs detached, different neighbourhoods — renting lets you experiment.

2.5 Credit, Income & Mortgage Qualification Reality

1. Not yet mortgage-ready

- Limited or poor credit history

- High existing debt

- New job or unstable income

Renting buys time while you improve your profile.

2. Self-employed or new to the country

Lenders may want 2+ years of income history. Rent while you build that.

3. High interest rate environment

Some folks consciously rent, waiting for mortgage conditions to become more favourable.

2.6 Risk Management & Strategy

1. Expecting a market correction

Some choose to rent because they truly believe prices are inflated and will fall.

2. Keeping options open

If you might move abroad, change careers, or go back to school, being locked into a large mortgage is not ideal.

3. Different investment preferences

Some people prefer to invest in their own business or diversified portfolios rather than piling everything into a house.

2.7 Personal & Life Stage Reasons

1. Separation or divorce

Renting can be a stabilizing “in-between” step while life is being rearranged.

2. Sold a home and not sure what’s next

Many people sell, rent for a year or two, then decide their next move with a clear head.

3. Seniors wanting simplicity

Less physical work, predictable costs, and the option to move closer to kids or healthcare.

4. Young adults gaining independence

Renting is often the first step out of the family home — long before homeownership is realistic or desirable.

2.8 Personal Preference

1. Not wanting to feel trapped

Some people genuinely hate the idea of a long-term, large loan and prefer the freedom of renting.

2. Prioritizing experiences over possessions

Travel, hobbies, education, or early-stage business building might matter more than owning.

3. Past bad experience as an owner

A nightmare renovation, big loss, or stressful sale can push someone back to renting long term.

4. Just not caring about owning

Not everyone sees owning as part of their identity or success. And that’s okay.

Hurdles of Renting (Including LTB/Eviction)

Renting has different hurdles than owning — not fewer.

For Ontario/Canada context, we’ll mention the Landlord and Tenant Board (LTB), but the general themes apply in many regions.

3.1 Eviction & Tenure Insecurity

Even excellent tenants can face termination:

- Landlord’s own use / buyer’s own use

Landlord or close family may want to move in, or the buyer wants the unit. There are rules, forms, compensation requirements, but from the tenant’s perspective, the bottom line is: you may have to move. - Demolition / conversion / major repairs

If the property will be demolished, converted, or requires vacant possession for major work, a tenancy can be terminated under specific legal frameworks. - Sale of the property

In many cases the lease survives a sale unless the buyer gives proper notice for personal use. But the uncertainty alone can be stressful. - Soft disputes escalating

Noise conflicts, parking disputes, alleged interference with “reasonable enjoyment” — these can become grounds for applications even when the situation feels grey.

The core hurdle: you never have the same level of control over staying put that an owner does.

3.2 LTB / Tribunal Delays and Complexity

On paper, landlord–tenant laws protect both sides. In practice:

- Backlogs

Hearings can take months. That means:- Slow remedies for repairs or harassment

- Long stretches living with uncertainty

- Complex procedures

Multiple forms (N-forms, T-forms), deadlines, rules of evidence, review processes — it’s a lot for someone without legal help. - Power imbalance

Larger or experienced landlords may be more familiar with the process than first-time tenants.

So a key hurdle of renting is that enforcing your rights can be slow, draining, and confusing, even when the law is technically on your side.

3.3 Rent Increases & Affordability

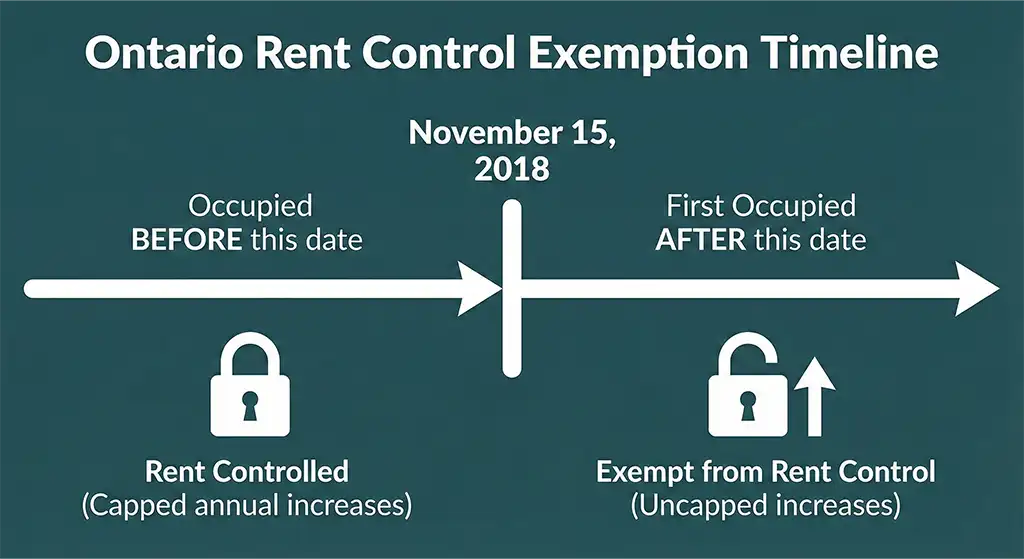

Rent Control vs. Exemptions (The 2018 Rule) Not all rentals in Ontario have rent control. This is a critical distinction for your budget:

- Rent Controlled: Most units occupied prior to November 15, 2018, are subject to the provincial guideline (e.g., capped at 2.5% in recent years).

- Exempt (Non-Controlled): New buildings, additions, or basement apartments that were occupied for residential purposes for the first time after November 15, 2018, are exempt from rent control.

If you rent a brand-new condo, the landlord can legally raise the rent by any amount (e.g., $500/month) once your initial 12-month term is up, provided they give proper notice (Form N2).

3.4 Maintenance & Habitability

Legally, landlords must keep properties in good repair. Reality is messier:

- Delayed or ignored repairs

Leaks, pests, heating issues, mold, broken appliances — tenants may wait weeks or months for action. - Fear of retaliation

Some tenants hesitate to push for repairs or file complaints out of fear of “rocking the boat” and seeing non-renewal or hostility. - Limited ability to self-fix

You can’t just replace wiring, walls, or windows on your own; even if you do, you likely won’t recoup that investment.

So the hurdle is: your living conditions depend heavily on how responsible your landlord is, and changing that reality is not simple.

3.5 Screening, Discrimination & Access

- Strict screening

Credit checks, income verification, references, guarantors — all can lock out:- Newcomers

- Young adults

- People with past credit issues

- People with informal or gig income

- De facto discrimination

Even with human rights protections, some tenants suspect (or know) they’re being filtered based on family size, race, disability, etc. It’s often subtle and hard to prove. - Competitive markets

In hot rental markets, tenants may feel pressured to:- Over-share personal information

- Offer above asking

- Accept unfavourable terms

Finding and securing a good rental can be a major hurdle, not a simple “just go rent something.”

3.6 Lease Clauses & Information Gaps

- Illegal/unreasonable clauses still show up in leases:

- “No guests ever”

- “No visitors after 9 pm”

- “You’ll automatically pay all landlord legal costs”

Some are unenforceable, but tenants may obey them anyway simply out of fear or lack of knowledge.

- Verbal promises vs written terms

“We’ll fix that before you move in” or “utilities are included” should be in writing. If they’re not, tenants may be left with their word against the landlord’s. - Unclear responsibility for utilities/maintenance

Fuzzy agreements can lead to surprise bills or conflict.

A key hurdle: information asymmetry. Many tenants simply don’t have the same knowledge or advice as landlords, especially professional ones.

3.7 Emotional & Practical Instability

- Feeling temporary, even after years in one place

- Kids being moved between schools when leases end or landlords change their plans

- Repeated moving costs: trucks, time off work, deposits, new furniture

At the extreme:

- Eviction for arrears after a short-term crisis

- Sheriff-enforced evictions, which are traumatic and hurt future rental prospects

- Informal lockouts, harassment, or pressure to sign “mutual terminations” under stress — all illegal, but they happen

All of this sits on the “renting” side of the scale when you ask, “Is renting or buying a house better for my situation?”

Hurdles of Owning a House

Owning isn’t “no problems.” It’s just a different set.

4.1 Upfront Financial Barriers

1. Big down payment

Saving 5–20% in an expensive market can take years and requires trade-offs with:

- Debt repayment

- Retirement savings

- Kids’ education

- Emergency funds

2. Closing costs

On top of the purchase price, buyers face:

- Land transfer tax (sometimes municipal + provincial)

- Legal fees

- Title insurance

- Inspection, appraisal

- Adjustments on taxes/condo fees/utilities

See List of Closing Costs typically associated with purchase of a home

- Land Transfer Tax (LTT): This is often the biggest surprise. In Toronto, you pay both Municipal and Provincial LTT.

- The Silver Lining: First-Time Home Buyers are often eligible for rebates (up to $4,000 for provincial and roughly $4,475 for Toronto municipal tax) to help offset this hit.

This can easily reach 1.5–4% of the purchase price.

3. Mortgage qualification

Lenders will scrutinize:

- Income stability

- Debt ratios

- Credit score

- Stress test at higher rates

Self-employed, new to country, or people with uneven income can struggle here.

4.2 Ongoing Monthly Load

1. Mortgage payment risk

You must make that payment every month — for years. Job loss, illness, or income changes can quickly become serious.

2. Interest rate risk

- Variable rate = payment or interest shock as rates change.

- Fixed rate = renewal risk; when your term ends, new rates might be much higher.

3. Property taxes, insurance, utilities

- Property taxes generally rise every year.

- Home Insurance: While not legally mandated by the government (like car insurance), almost every mortgage lender will require you to have full fire/hazard coverage before they release funds.

- Utilities for a larger space (heating a whole house vs. a condo) can be a shock to the budget.

4. Condo/HOA fees (if applicable)

- Monthly fees for shared amenities and maintenance

- Potential for increases

- Risk of special assessments for major projects

Being “house poor” — where most of your income goes to the mortgage and house costs — is a very real hurdle.

4.3 Maintenance & Big Repairs

1. Routine maintenance

You’re responsible for:

- Snow and yard care

- Cleaning gutters

- Servicing furnace/AC

- Addressing minor leaks and wear-and-tear

That’s time, money, and planning.

2. Capital expenditures (“surprise” big bills)

- Roof replacement

- Furnace/AC

- Windows and doors

- Foundation fixes

- Sewer issues

- Major appliances

Any one of these can be $5,000–$30,000+. There’s no landlord to call.

3. Renovation risks

- Projects that go over budget and over time

- Contractors who do poor work or disappear

- Hidden issues discovered mid-reno (mold, asbestos, wiring)

Renovation stress can be very real on relationships and mental health. While your mortgage principal is fixed, property taxes, insurance, and repair costs usually rise annually with inflation.

4.4 Market & Equity Risk

1. Price volatility

Home values don’t only go up. They can stagnate or fall, especially in specific segments or neighbourhoods.

2. Being trapped by the market

- If you must move (job change, divorce) in a down market, you may face a loss or have trouble selling quickly.

- You might be forced to carry two properties temporarily or rent one out in a hurry.

3. Concentration risk

For many households, the house is the bulk of their net worth. If something goes wrong with that one asset (market, environmental risk, neighbourhood decline), it hits hard.

4.5 Liquidity & Flexibility Costs

1. Expensive to move

Selling usually involves:

- Real estate commissions

- Legal fees

- Mortgage penalties (depending on term/type)

- Moving costs

2. Less mobility for work or life changes

You can’t just give notice and leave. That can affect career decisions, family choices, and lifestyle flexibility.

3. Opportunity cost

The money tied up in down payment, closing costs, and principal payments is not easily accessible and might have earned more elsewhere — or given you more options — in some scenarios.

4.6 Legal, Compliance & Liability

1. Permits and bylaws

- Structural, plumbing, or electrical work often needs permits.

- Skipping permits can cause issues with insurance, fines, and resale.

2. Old or unsafe building issues

- Asbestos, knob-and-tube wiring, lead paint, outdated electrical panels

- Fixing these can be expensive and sometimes mandatory for safety or insurance.

3. Liability as an owner

- If someone is injured on your property, you can be held responsible.

- Home insurance helps, but you still have a duty to maintain safe conditions.

4. Condo/HOA governance

- Mismanaged reserve funds

- Internal politics

- Surprise special assessments

Even as an owner, you can be dragged into disputes and costs you didn’t expect.

4.7 Emotional & Relationship Stress

1. Financial stress between partners

- Disagreements over budget, renovations, upgrades, or how much to borrow

- Arguments when money gets tight

2. Renovation stress

Dust, noise, delays, and constant decision-making can strain even strong relationships.

3. Responsibility fatigue

Many owners feel like there is always something that needs attention — which can be exhausting over time.

4.8 Neighbourhood & Environmental Risks

1. Difficult neighbours

If the people next door are noisy, aggressive, or constantly in conflict, escaping that environment is harder when you own.

2. Changing neighbourhood

- More traffic

- New high-density developments

- Rising crime

- Changes to schools or amenities

You’re tied to the area more than a renter is.

3. Climate and environmental risk

- Flood zones, wildfire areas, erosion

- Insurance costs rising or coverage limits changing

These can affect both quality of life and resale value.

4.9 If You Rent Out Part of Your Home

1. Landlord responsibilities

By “house hacking,” you now carry both owner and landlord hurdles:

- Non-payment risk

- Tenant damage

- Tribunal/LTB delays if you need to enforce anything

2. Regulatory complexity

Rules on:

- Secondary suites

- Fire code and building code

- Short-term rentals

A misstep here can mean fines or being ordered to shut down a rental unit.

4.10 The Mortgage “Stress Test”

In Canada, qualifying for a mortgage isn’t just about affording the monthly payment at today’s rate. You must pass the federal Stress Test.

You must prove you can afford the mortgage at:

- The rate offered by your bank + 2%, OR

- 5.25% (whichever is higher).

This reduces your “buying power.” Even if you have the down payment, the Stress Test might limit the amount you can borrow, forcing you to look at smaller homes or different neighbourhoods than you initially planned.

Note: As of late 2024, First-Time Home Buyers may be eligible for a 30-year amortization period (instead of the standard 25 years) on insured mortgages, which can lower monthly payments and help with qualification.

Renting vs Owning: Side-by-Side

A neutral comparison of home ownership vs renting so you can see the trade-offs, not a “right” or “wrong” answer.

| Area | Renting a Home | Owning a Home |

|---|---|---|

| Upfront Money |

Renter

Lower: first/last, deposits, moving costs.

|

Owner

Higher: down payment + closing costs (tax, legal, inspections, etc.).

|

| Monthly Costs |

Renter

Rent + utilities + tenant insurance. No big repair bills, but rent may rise at renewal.

|

Owner

Mortgage + taxes + insurance + utilities (+ condo/HOA fees). Payments can jump on renewal if rates rise.

|

| Repairs & Maintenance |

Renter

Landlord handles major repairs. Less control over timing/quality.

|

Owner

You handle (and fund) all repairs and maintenance. More control, but more responsibility.

|

| Flexibility |

Renter

Easier to move cities/neighbourhoods. Ending a lease is usually simpler than selling.

|

Owner

Harder and more expensive to move. Selling involves time, market risk, and fees.

|

| Control Over Space |

Renter

Limited ability to customize. Need permission for many changes.

|

Owner

Broad control to renovate, decorate, and modify (subject to bylaws/code).

|

| Stability |

Renter

Potential for landlord-driven moves (sale, own use, renos).

|

Owner

Stronger control over staying — as long as you can afford the home.

|

| Financial Upside/Downside |

Renter

No equity, but no housing-market risk or repair risk. May invest savings elsewhere.

|

Owner

Equity growth + potential price appreciation, but also market risk and big-ticket repair risk.

|

| Lifestyle Fit |

Renter

Good for shorter timelines, uncertain plans, or if you value mobility.

|

Owner

Good for long-term plans, stable roots, and deep customization of your home.

|

| Psychological Load |

Renter

Less “house” responsibility, but potential uncertainty about future housing.

|

Owner

Stability and pride of ownership, with more ongoing responsibility and stress.

|

This table shows general patterns only. Actual costs, protections, and responsibilities vary by province/state, building type, and your specific lease or mortgage.

| Area / Issue | Hurdles When Renting | Hurdles When Owning |

|---|---|---|

| Security of Tenure |

Renter risk

Risk of eviction for landlord’s own use, sale, renos, or disputes. Forced moves possible.

|

Owner risk

Risk of default, forced sale, or foreclosure if you can’t keep up with payments or taxes.

|

| Legal / Process |

Renter risk

Navigating LTB/tribunals for repairs or disputes; backlogs and stress.

|

Owner risk

Navigating permits, bylaws, code, condo rules; risk of fines or forced changes.

|

| Affordability Over Time |

Renter risk

Rent increases, new fees, utilities added to your load.

|

Owner risk

Rate resets, tax increases, rising insurance, increasing maintenance costs.

|

| Control Over Conditions |

Renter risk

Dependent on landlord for repairs, maintenance, and rule enforcement.

|

Owner risk

Fully responsible for condition and safety of the property.

|

| Mobility |

Renter risk

Shorter notice needed but must secure a new place in competitive markets.

|

Owner risk

Selling and moving is slow and expensive; your life is more anchored.

|

| Worst-Case Scenario |

Renter risk

Eviction, sheriff involvement, difficulty renting again.

|

Owner risk

Foreclosure/power of sale, major loss of equity, or being stuck with a distressed property.

|

Both sides have real risks. The question isn’t “Is renting or buying a house better?” It’s: which risk profile fits your life and comfort level right now — the renter’s risks or the owner’s risks?

Mortgage vs Rent: How to Think About the Numbers

Instead of just comparing a mortgage payment to rent, look at the whole picture: monthly cash flow, time horizon, what you do with any “savings,” and how much risk and uncertainty you’re comfortable carrying.

Start by building a simple, realistic monthly picture for both renting and owning. Include ongoing costs you might otherwise forget.

- Mortgage payment (principal + interest)

- Property taxes

- Home insurance

- Maintenance fund (even a placeholder like 1–2% of home value per year)

- Condo/HOA fees, if any

- Home utilities (heat, hydro, water, internet, etc.)

- Monthly rent

- Tenant insurance

- Utilities you pay directly (hydro, internet, etc.)

- Any parking, storage, or service fees

- Small repair or move-out costs your lease assigns to you

Once you have both totals, you’re comparing full monthly cost to full monthly cost — not just “rent vs mortgage payment,” which can be misleading.

How long you expect to stay in one place is a key part of the rent vs buy decision. Transaction costs can tilt the math.

- If you’re likely to move in under ~5 years, renting can often be more efficient.

- While both parties incur expenses like legal fees and moving costs, the financial obligations differ significantly. Buyers are typically responsible for land transfer taxes and inspections, whereas Sellers generally cover realtor commissions and mortgage discharge fees.

- Those one-time costs are spread over a short period, which can eat into any equity you build.

- Over longer horizons, ownership has more time to spread out transaction costs and benefit from potential price appreciation.

- You also have more years for each mortgage payment to shift from mostly interest to more principal (equity).

- A longer stay can make it easier to justify upfront closing costs and ongoing ownership expenses.

There is no fixed “right” number of years — this is a guideline to help frame the trade-off between flexibility and the long-term benefits of owning.

Renting only “wins” financially if you consistently invest the money you’re not spending on ownership costs — not if it just disappears into day-to-day spending.

- You deliberately invest the difference between your total rent cost and total ownership cost.

- You choose investment vehicles that match your risk tolerance and time horizon (e.g., diversified funds, a TFSA/RRSP in Canada).

- You treat those monthly investments as non-negotiable, just like a mortgage payment.

- If the “savings” from renting are regularly absorbed by lifestyle spending, the financial advantage shrinks.

- Ownership forces some saving through mortgage principal payments — renting doesn’t, unless you build that discipline yourself.

- Being honest about how you actually manage money is just as important as what a spreadsheet says.

A calculator can model different investment returns, but your real behaviour over time is what ultimately drives outcomes.

The “best” choice on paper might not be the best choice for your stress levels. Risk and uncertainty carry a real emotional cost.

- Ownership risk: Big, irregular repair bills; mortgage rate increases; property tax or insurance hikes.

- Renting risk: Being asked to move due to landlord decisions (sale, own use, renovations) or changes to your lease.

- If either scenario would keep you up at night, that is a meaningful cost — not just a “feeling.”

There is no one-size-fits-all answer. A slightly more expensive option might still be the right choice if it gives you a level of stability or flexibility that aligns better with your life.

House for Lease vs Rent vs Buy: What Are You Really Choosing?

When you see ads like “house for lease”, “for rent”, or MLS listings for sale, what you’re really choosing between is:

- Shorter-term commitment (lease/rent)

- Long-term commitment (mortgage/ownership)

A house for lease vs rent is mostly about contract wording and term length. The bigger decision is:

- Do I want long-term flexibility? (rent/lease)

- Or long-term control and responsibility? (buy/mortgage)

How to Decide: Key Questions to Ask Yourself

There is no universal “best” choice — only the best choice for you, right now. Use these questions as a reality check:

1. How long am I likely to stay in this city/neighbourhood?

Under 3–5 years → renting often makes more sense.

5+ years with stable plans → ownership may be worth exploring.

2. How stable is my income?

Is it steady and predictable?

Could I handle a rate increase or temporary job loss?

3. Do I have (or can I build) a buffer?

Emergency fund

Room in my budget for repairs or rent increases

4. How do I feel about responsibility vs flexibility?

Do I like fixing and improving things, or does that idea exhaust me?

Does moving every few years sound exciting or stressful?

5. What matters more right now: roots or options?

Young, mobile, exploring careers or cities → renting may be a better fit.

Kids, schools, caregiving, community ties → buying may align better.

6. If I buy, will I still be able to:

Save for retirement?

Handle family needs?

Enjoy life (travel, activities), or will I feel “house poor”?

7. If I keep renting, will I actually invest the difference?

If not, the financial advantage of renting may be smaller than it appears.

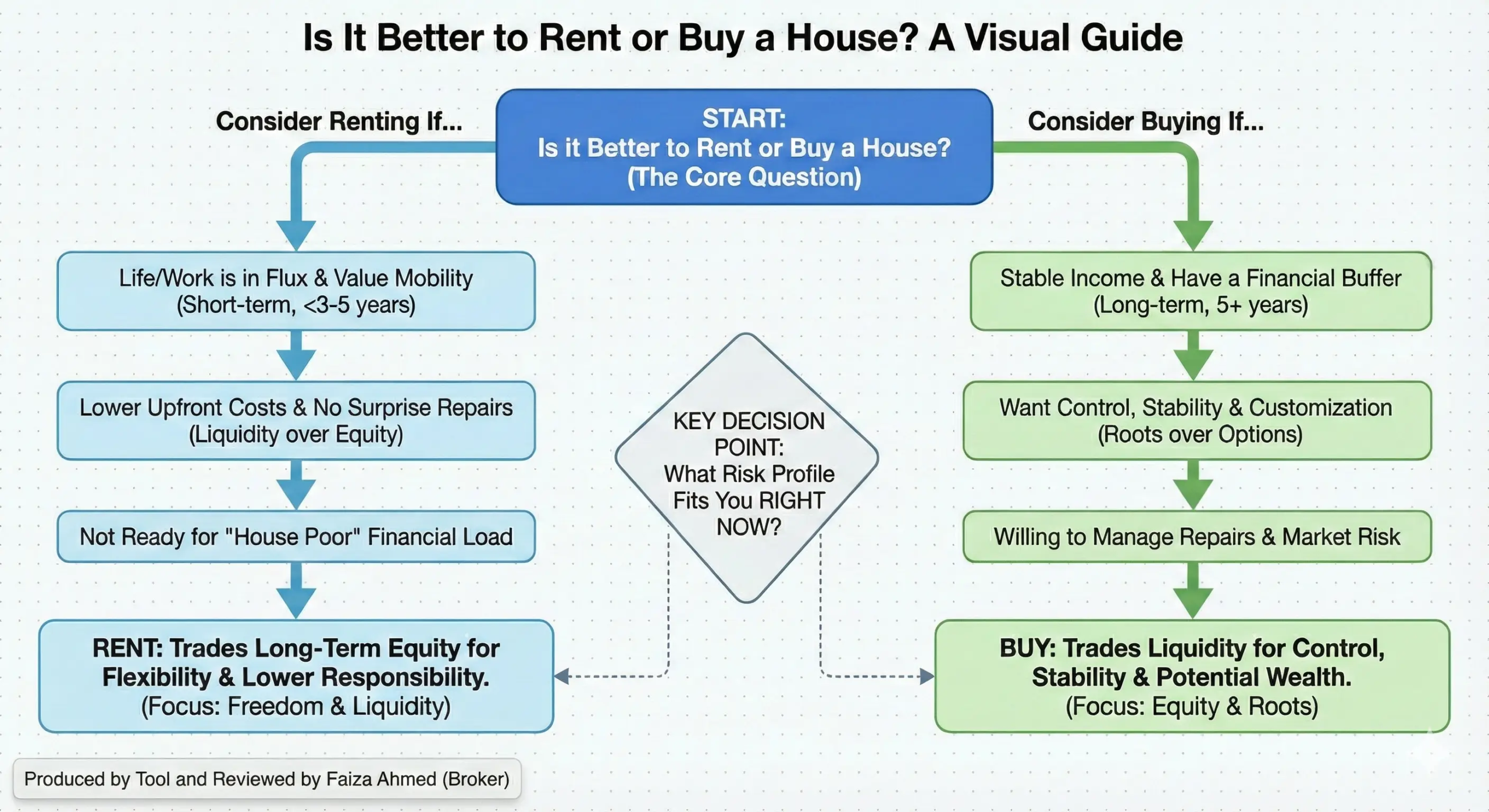

So… Is It Better to Rent or Buy a House?

You can see now why “is it better to rent a house or buy?” doesn’t have a one-size-fits-all answer.

- Owning is usually better if:

- You have stable income and a buffer

- You plan to stay put for several years

- You want control, stability, and the chance to build equity

- You’re willing to take on maintenance, repairs, and market risk

- Renting is usually better if:

- Your life or work situation is in flux

- You value mobility and flexibility

- You don’t want (or can’t yet handle) the financial and emotional load of ownership

- You’re prepared to save and invest the money you’re not tying up in a house

In other words:

Renting trades long-term equity for flexibility and lower responsibility. Owning trades flexibility and liquidity for control, stability, and potential long-term wealth.

Once you’re clear on which trade-off matters more for you, right now, the decision — while still big — becomes a lot less confusing.